Citi Targets 5.5% on 30-Year Treasury as 'Big Beautiful Bill' Adds $3.5 Trillion to U.S. Deficit

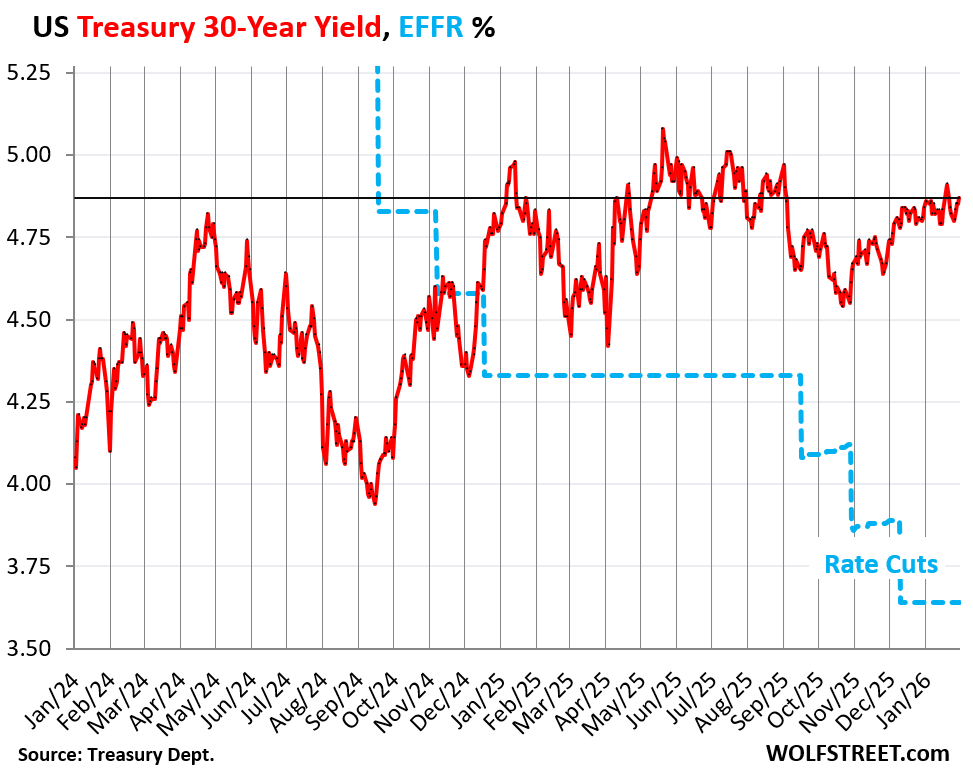

The bond market is not done repricing American fiscal risk. After the 30-year U.S. Treasury yield surged past 5.2% — its highest level since 2007 — Citigroup's analysts have named 5.5% as the next key technical and psychological level to watch, according to Bloomberg reporting from May 19.

The move from 5.2% to 5.5% may sound small. In bond market terms, it is seismic. At those yield levels, every additional basis point represents hundreds of billions of dollars in higher annual borrowing costs for the federal government — and cascading increases in mortgage rates, corporate bond spreads, auto loan rates, and commercial real estate refinancing pressures.

What's Driving the Move: Three Converging Forces

The 30-year yield's surge above 5% was not triggered by a single event. It is the convergence of three pressures that have been building since early 2025:

The Iran War Energy Shock. The closure of the Strait of Hormuz cut off approximately 20% of global oil supply. Consumer prices rose 3.8% year-over-year in April 2026, and the Producer Price Index surged 6.0%. Bond investors demand higher nominal yields to compensate for inflation eating into real returns — and with no clear path to Hormuz reopening, inflation expectations remain elevated.

The Fiscal Deterioration. The fiscal 2026 deficit is on track to reach $1.89 trillion — the gap between $7.4 trillion in spending and $5.5 trillion in revenues, according to JPMorgan's analysis. Federal debt has now crossed 101% of GDP, a threshold not breached since World War II. The U.S. is now spending more to service its debt than to fund national defense or Medicare — a milestone that investors and credit rating agencies are treating as a structural warning.

The Big Beautiful Bill. The American Enterprise Institute and the Congressional Budget Office have confirmed that Trump's signature domestic legislation — the "One Big Beautiful Bill Act" — will add $3.5 trillion to the budget deficit over the next decade. The bill extends and expands tax cuts while leaving entitlement spending intact. The bond market reacted immediately: yields spiked on each successive Senate vote, and Moody's downgraded U.S. sovereign credit, citing long-term fiscal trajectory.

JPMorgan's Five Scenarios: Even the Best Case Is Alarming

David Kelly, JPMorgan's chief global strategist, published an analysis mapping five distinct paths for U.S. debt over the next decade. The conclusion: even his most optimistic scenario ends with federal debt at 115% of GDP by 2036, up from roughly 101% today.

Federal debt surged from 31% of GDP in 2001 to 101% today — driven by "unfunded tax cuts, stimulus checks, and wars rather than prolonged economic underperformance," Kelly wrote. The Big Beautiful Bill's passage has pushed every scenario further into uncharted fiscal territory.

Kelly's most pessimistic scenarios involve a fiscal crisis — a moment when the Treasury cannot find sufficient buyers for its debt at any yield the government can sustain — that could arrive as early as 2029–2031.

The 5.5% Threshold: What It Means

Citi's analysis of the 5.5% level focuses on a specific structural problem. The 2-year Treasury yield has already crossed above the Fed's 3.70–3.75% upper target range, meaning the bond market is pricing in rate hikes before the FOMC has voted for any. A Bank of America survey found that 62% of global fund managers expect 30-year yields to hit 6% — a level not seen since 1999.

At 5.5%, the 30-year yield would begin to exert consistent drag on equity valuations through discounted cash flow mathematics. It would push the 30-year fixed mortgage rate toward 7.5% or higher, effectively ending the already-frozen housing market. And it would drive commercial real estate refinancing costs to levels where the math on existing loan structures — originated when rates were 3–4% — simply no longer works.

The Bank of America's HSBC analysts have already named the 5%+ zone on the 30-year the "danger zone." At 5.5%, the danger becomes systemic rather than episodic.

The Global Context

The U.S. is not alone. The 30-year UK Gilt yield hit its highest since 1998. Germany's long-term borrowing rate is at a 15-year high. Japan's 30-year bond yield hit a record. When every major sovereign bond market is selling off simultaneously, it signals something more than domestic policy error — it signals a global repricing of the risk premium on long-duration government debt.

The question bond investors are wrestling with is whether this repricing is temporary — driven by the Iran conflict and expected to reverse when the war ends — or structural, reflecting a permanent shift in how markets view the creditworthiness of heavily indebted governments. The passage of the Big Beautiful Bill has strengthened the case for the structural view.

Protect Your Portfolio From Bond Market Risk

These books offer essential frameworks for understanding and navigating a prolonged bond market downturn:

- Currency Wars by James Rickards — How sovereign debt crises and currency conflicts reshape global financial markets.

- The Bond King by Mary Childs — A definitive account of how bond markets work and what happens when they break.

- Crash Proof 2.0 by Peter Schiff — A guide to protecting and growing wealth when dollar-denominated assets are under pressure.

Sources: Bloomberg, CNBC, Fortune, American Enterprise Institute, Wall Street Journal, Financial Times